Highest Interest Rates Paying Small Finance on Fixed Deposits

Higher interest paying banks on FD

What is Fixed deposits (FD)?

A fixed deposit (FD) is a tenured deposit account provided by small finance, banks or non-bank financial institutions which provides investors a higher rate of interest than a regular savings account, until the given maturity date. It may or may not require the creation of a separate account. Higher interest paying banks on FD with various benefits are explained below.,

FD interest rates in July 2024: Many banks have revised their fixed deposit interest rates effective July 1, 2024 for amounts below Rs 3 crore. Note that some banks have updated the date and rates remain the same. Check which bank offers the highest interest rates after the revision.

Small Finance Bank Fixed Deposit Rates

- Fixed deposits are one of the most popular modes of investment in India. Fixed deposits are considered to be risk-free investments that guarantee assured returns on maturity with attractive interest rates.

- Flexible tenures ranging from 7 days to 10 years, and tax benefits for the category of Tax Saver FDs which have a tenure of 5 years. Banks, Non-Banking Finance Companies (NBFCs), and small finance banks offer fixed deposit facilities in India.

Benefits

- Customers can avail loans against FDs up to 80 to 90 percent of the value of deposits. The rate of interest on the loan could be 1 to 2 percent over the rate offered on the deposit.

- Residents of India can open these accounts for a minimum of seven days.

- Investing in a fixed deposit earns customers a higher interest rate than depositing money in a saving account.

- Tax saving fixed deposits are a type of fixed deposits that allow the investor to save tax under Section 80C of the Income Tax Act.

Simple to Understand

As safe an option FD is, it is equally easy to comprehend too. For an amount of Rs. 1 lakh for 1 year @ 8% interest, there will be a profit of Rs. 8,243 (quarterly compounding). No market fluctuation shall bring this amount down. There is no need to monitor the FD on a daily basis, unlike other investment instruments like equity funds. There are no market-related dips involved in FD.

Who should Invest in Fixed Deposits?

- If you’re someone who does not want to take market-related risks and is okay with decent returns, FD will work well for you.

- If you have taxable income and are looking for a tax-saving safe investment option, you should consider FD. It will allow you up to Rs. 1.5 lakh of Income Tax Deductions u/s 80C of the IT Act.

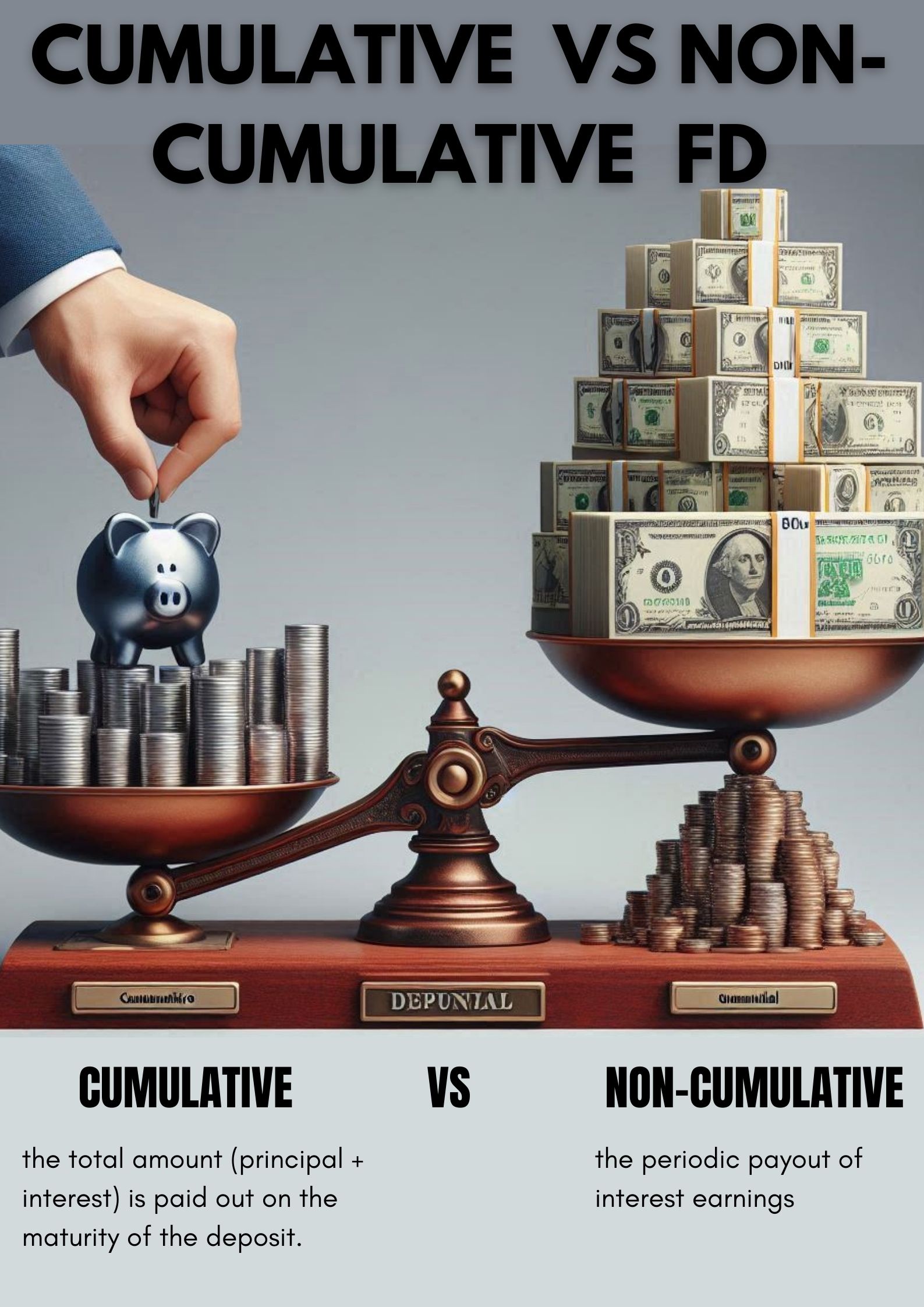

- If you’re a retired person who wants a regular income, invest your savings in different FD schemes across various banks and go for the non-cumulative option. In this option, you will get the regular interest that will act as your income post-retirement.

- If you’re a housemaker who has a certain amount to invest, it would be good for you to analyse the FD option. This is because fixed deposits do not carry any significant risk.

- Higher interest paying banks on FD, when ever getting FDs are classified into two cumulative and non cumulative FDs. where as returns for cumulative FDs are bit higher than the non-cumulative FDs.

Scheduled Banks offering highest FD interest rates – 6.50% p.a. and above

Amongst all bank categories, small finance banks are offering the best FD interest rates. Higher interest paying banks on FD Within the scheduled small finance bank category, Unity Small Finance Bank and North East Small Finance Bank offer the highest FD interest rate of 9.00% p.a. Among scheduled private sector banks, SBM Bank offers the best FD interest rates of up to 8.40% p.a. for a tenure of above 3 years 2 days to less than 5 years. Among scheduled public sector banks, Punjab & Sind offers the highest fixed deposit interest rates of up to 7.30% p.a. on tenure 666 days.

Here are banks and higher interest rates according to tenure

| Banks | Highest FD rate (% p.a.) |

1-year FD rate (% p.a.) |

3-year FD rate (% p.a.) |

5-year FD rate (% p.a.) |

Additional interest rate for senior citizens (% p.a.) |

| Unity Small Finance Bank | 9.00 | 7.85 | 8.15 | 8.15 | 0.50 |

| North East Small Finance Bank | 9.00 | 7.00 | 9.00 | 8.00 | 0.50 |

| Suryoday Small Finance Bank | 8.65 | 6.85 | 8.60 | 8.25 | 0.24-0.50 |

| Shivalik Small Finance Bank | 8.55 | 7.80 | 7.50 | 6.50 | 0.50 |

| Equitas Small Finance Bank | 8.50 | 8.20 | 8.00 | 7.25 | 0.50 |

| Utkarsh Small Finance Bank | 8.50 | 8.00 | 8.50 | 7.75 | 0.60 |

| Jana Small Finance Bank | 8.25 | 8.25 | 8.25 | 7.25 | 0.50 |

| Ujjivan Small Finance Bank | 8.25 | 8.25 | 7.20 | 7.20 | 0.50 |

| ESAF Small Finance Bank | 8.25 | 6.00 | 6.75 | 6.25 | 0.50 |

| DCB Bank | 8.05 | 7.10 | 7.55 | 7.40 | 0.50 |

| RBL Bank | 8.00 | 7.50 | 7.50 | 7.10 | 0.50 |

| AU Small Finance Bank | 8.00 | 7.25 | 7.50 | 7.25 | 0.50 |

| Induslnd Bank | 7.99 | 7.75 | 7.25 | 7.25 | 0.26-0.50 |

| IDFC First Bank | 7.90 | 6.50 | 7.25 | 7.00 | 0.50 |

| Bandhan Bank | 7.85 | 7.85 | 7.25 | 5.85 | 0.50-0.75 |

| SBM Bank | 7.75 | 7.05 | 7.30 | 7.75 | 0.50 |

| YES Bank | 7.75 | 7.25 | 7.25 | 7.25 | 0.50-0.75 |

| Punjab & Sind Bank | 7.30 | 6.30 | 6.00 | 6.00 | 0.50 |

| Punjab National Bank | 7.25 | 6.75 | 7.00 | 6.50 | 0.50 |

| Bank of Baroda | 7.25 | 6.85 | 7.25 | 6.50 | 0.50-1.00 |

Fixed deposits (FDs) are a popular investment option, Higher interest paying banks on FD especially for those seeking safety and predictable returns. Here are the advantages and disadvantages of fixed deposits:

Advantages:

- Safety: Fixed deposits are considered one of the safest investment options since they are not subject to market risks. Most banks offer insurance on fixed deposits up to a certain limit (e.g., in the US, the FDIC insures deposits up to $250,000).

- Guaranteed Returns: The interest rate is fixed at the time of investment and remains constant, ensuring a predictable return.

- Flexible Tenures: Fixed deposits come with flexible tenure options, ranging from a few months to several years.

- Higher Interest Rates than Savings Accounts: Fixed deposits generally offer higher interest rates compared to regular savings accounts.

- Tax Benefits: In some countries, certain types of fixed deposits qualify for tax benefits under specific sections of the income tax laws.

- Loan Against FD: Investors can avail of loans against their fixed deposits, providing a way to access funds without breaking the FD.

Disadvantages:

- Lower Returns Compared to Other Investments: Fixed deposits typically offer lower returns compared to other investment options like stocks, mutual funds, or real estate.

- Penalties for Premature Withdrawal: Withdrawing the fixed deposit before maturity usually incurs a penalty, reducing the overall return.

- Taxable Interest: The interest earned on fixed deposits is generally subject to tax, which can reduce the effective return.

- Lack of Diversification: Investing a large portion of funds in fixed deposits can lead to a lack of diversification in an investment portfolio.

- Interest Rate Risk: In a rising interest rate environment, the fixed rate on an FD may become less attractive compared to new FDs offering higher rates.

Overall, fixed deposits are suitable for risk-averse investors looking for stability and guaranteed returns. However, they may not be the best option for those seeking higher returns and willing to take on more risk.

Read more about Fixed Deposit Types of Cumulative vs non-cumulative FDs

Taxs saving on Fixed Deposit (FD)

Other articles on Fixed Deposit FD